In order to understand what Central Banks did wrong, leading up to both crises, and are still doing wrong it is necessary to consider a few preliminary points.

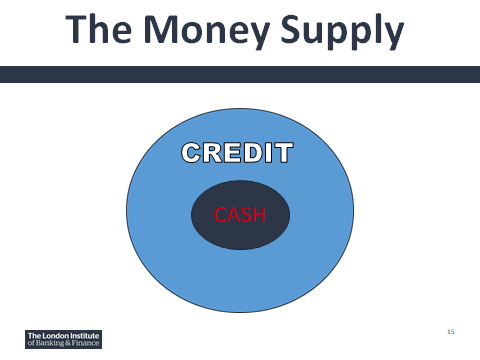

Modern money is fiat money (backed by nothing other than itself) and composed of a small inner core of cash/legal tender and an outer ring of credit created money. Together they make up the money supply as illustrated below and it may help at this point to focus on the TWO RINGS OF MONEY

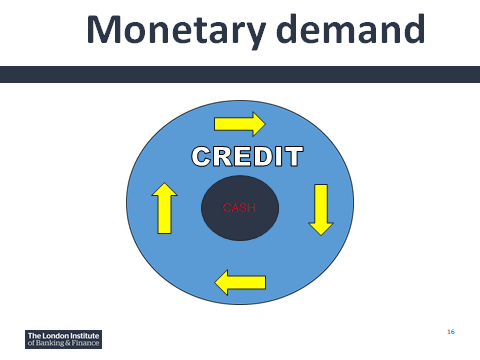

It is relatively easy to measure the money supply at one point in time. As the supplier of cash the Central Bank can approximate the amount of notes and coins in the economy. Other banks can supply information regarding the quantity of current or checkable accounts from which people could make immediate purchases. Think of the total as an inactive, slice in time, quantity of money (M) in the economy. To make it active over time we need to know the number of times on average each unit of money is used in transactions. This is the speed it has circulated over a given period of time or its velocity (V) and is illustrated below as monetary demand

A modern Central Bank has total control over the quantity of cash in the monetary system as it prints and mints the currency. It has much less control over that component of money which is determined and created by bank lending and it has almost no control over the speed that money is passed around in the economy.

Over a given period of time the money supply (stock of money) multiplied by the speed it is passed on will equal the average price level multiplied by the number of transactions completed in the economy. This is represented by the quantity theory of money equation M x V = P x T. As a simple example if there was £500 of transactions (P x T) over a given period of time and there was a 100 units of money in the economy then on average each unit of money has been passed around 5 times (M x V).

Before we look at the crises (GFC & GEC) take note of the fact that monetary policy is about managing the amount of monetary demand in the economy. To do this the Central Bank has two main levers of control. Firstly it can manipulate the cash component of money where a simple example is quantitative easing (QE). This will increase the inner ring of money or alternatively quantitative tightening (QT) will reduce the size of the inner ring. Secondly the Bank can manipulate the official interest rate (Bank Rate, Refi Rate, Fed Funds Rate) and encourage more demand for bank lending by lowering rates or less demand for bank lending by raising rates. This increases or decreases the outer credit created ring of money.

Hold the image of two rings of money in your mind as we look at each crisis.

The Global Financial Crisis

The GFC was caused from the USA. Between 1998 -2006 the US government artificially sponsored a boom in house prices. Federal Reserve Chairman Greenspan lowered Fed Funds Rate to make mortgages cheaper, Fannie May and Freddic Mac were Government Sponsored Enterprises who guaranteed to buy up all loans issued by Mortgage Brokers. There was affirmative action for disadvantaged groups, 100% loan to value mortgages, self declarations, tax breaks and teaser rates. All together these incentives to buy produced a housing boom.

Imagine this situation: a mortgage broker sees a couple looking at a house and asks them if they would like to buy it. They ask how much the mortgage would be. The answer is $3000 pm and the couple say they cannot afford that, the most they can afford is $1000 pm. That`s a coincidence says the mortgage broker I can offer you a teaser rate for 2 years costing you $1000 pm. The couple think and say that after two years they will not be able to afford the $3000. No worries says the broker if you cannot afford to continue then the house will be repossessed the mortgage repaid and as house prices are rising by 10% a year you will have a nice sum to put down as a deposit on a new home. It will be the best investment you ever made and start you climbing the property ladder. Who could resist this win/win offer?

On top of this booming property market was a derivatives market where a Mortgage Backed Security (MBS) was being traded and new securities were being created as Collateralized Debt Obligations (CDO`s) and synthetic CDO`s. The markets were new and regulations were weak as the Fed was not keeping up with these innovative products that were little more than fostering speculation and gambling dependent upon level of knowledge. Gradually the more informed professionals were beginning to see that the true value of bundles of securitised assets were overvalued and vulnerable to a downgrade. They started betting on these products failing by taking out Credit Default Swaps. Two good reads explain this: The Devil`s Derivatives by Nicholas Dunbar and Meltdown by Thomas E Woods Jr and if you prefer a good film, The Big Short, documents these events well.

Housing repossessions started, house prices fell, securitised bundles of mortgages were not being sold and toxic mortgages were being uncovered in these assets. Fannie and Freddie went into Conservatorship (liquidation), banks were receiving financial support and Ratings Agencies started to downgrade property assets. On September 15th 2008 the financial crisis was triggered when Lehman Brothers filed for bankruptcy.

The day after Lehman fail the interbank market froze in a “Who`s next” frenzy, stock markets fell, more toxic assets are exposed, Iceland fails financially, RBS and Lloyds are bailed out in the UK and Goldman Sachs and Morgan Stanley change their status from investment banks to retail banks so they can access bail-out funds. Money supply and monetary demand contract threatening what was thought to be a coming deflation to match the Great Depression. At this point Central Banks act. Their first attempt was to expand the outer ring of money by lowering the official interest rate to almost ZIRP (zero interest rate policy). This did not work as banks were more concerned about a possible liquidity crisis and were already contracting net lending to hold proportionally more cash. The second attempt by Central Banks was more successful as they pumped cash into the inner money ring through a quantitative easing process (QE) that saw them buying back second hand government debt.

QE was relatively successful in avoiding deflation and as no one knew the right amount of money to print, and more was better than less, inflation rose above target (just under 6% RPI in the UK). ZIRP was an unmitigated disaster. It did not have the desired effect on lending. Instead it distorted interest rates at the secure end of the interest rate spectrum, created speculative asset bubbles in stock and property markets and promoted unproductive investment in flipping second hand assets. Even worse it created a situation where no country on its own can get out of ZIRP without creating unbearable volatility in exchange rates and at present there is no indication that Central Banks will come together to get themselves out of this problem.

The Global Economic Crisis

The world was then left in a fragile economic state and a new crisis was looming. Expansionary monetary policies were not working and since a G20 London meeting in March 2009, where it was agreed that all countries pursue expansionary fiscal policies, we have seen waste, resources misallocated, growth rates fall and productivity gains almost eliminated. For more than a decade the only growth area has been in government talking about how to solve problems while squeezing the economic life blood out of the private sector.

Lehman Brothers was the first trigger for a crisis while Covid19 was the second trigger for the next crisis. This time it was not just a GFC as it had became a GEC where output is contracting, unemployment is rising and desperate governments and their Central Banks have no room to manoeuvre on interest rates. The result is that fiscal policies are causing ever larger government overspending and borrowing requirements at a time when tax takes are falling. To understand what is going to happen next we need to focus our attention on the two rings of money, the money stock (M) and the speed it is being passed around (V).

It is not necessary to have a PhD to realise that the velocity of circulation of money is slowing as lockdown is keeping people inside with much less opportunity to spend, or pass on money. At the same time Central Banks are saying that they will do whatever it takes and as there is only one option we are being given more QE. They have no alternative but to buy government debt and print money. This means that under present circumstances monetary policy is faced with two opposing forces. The stock of money is being expanded but the speed it is going round is slowing. I have explained in other blog articles that the only cause of a change in average prices, inflation or deflation, is the rate at which monetary demand (M x V) grows. Also we need to take account of a time lag as an expansion in money supply now will not feed through to prices for anything between about nine months and two years dependent upon the stability of the economy`s starting position.

Given that we are currently seeing opposing forces the change in average prices over the next nine months will be indeterminate, a small rise or fall, but after we return to the “new normal” then both forces will be moving in the same direction and inflation will pick up to higher rates that have not been seen in the last 30 years. Therefore we must expect a bumpy ride as politicians will require to be advised that they can spend more money and Central Banks will accommodate that with printed money. The only way to see a sustained recovery is to hope that the inflation works its way through the economy without too much disruption and that people accept an explanation that it has been caused by greedy bankers, profit seeking entrepreneurs, intransigent unions, the falling exchange rate and of course Covid19.

All we need to remember is that inflation and deflation can only ever be caused by a Central Bank who must be judged only by their record of maintaining stable prices through their monetary policy.

John Hearn 15/5/2020

How far can the tertiary sector be developed?

LikeLike

The sky is the limit. The manufacturing sector will expand using more robotics and AI releasing more and more people to work in the service sector where personal service is requested and rewarded.

LikeLike